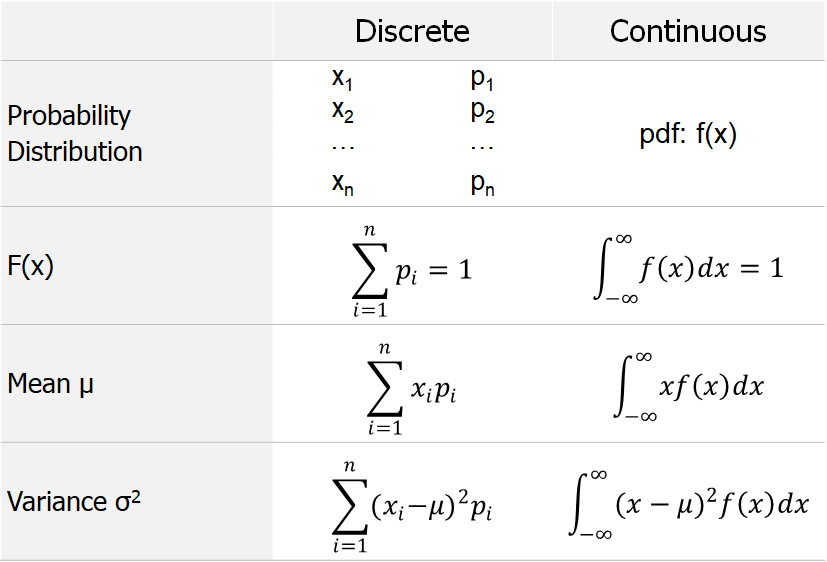

Exhibit 34.14 Comparison between discrete and continuous distributions.

A comparison between discrete and continuous probability distributions is given in

Exhibit 34.14. The probability distribution of a continuous random variable, X, is described

by its probability density function (pdf), f(x).

$$Mean \,μ = \int_{-∞}^∞ x f(x)dx$$

$$Variance \,σ = \int_{-∞}^∞ (x-μ)^2 f(x)dx$$

For a given time, t, the cumulative distribution function (cdf) F(t) of a

continuous random variable, X, is defined by:

$$F(t)=P(X≤t)=\int_{-∞}^t f(x)dx$$

$$F(-∞)=0,\,F(∞)=1 $$